For:

We will build a SARIMAX model for monthly data on an industrial production time series for the 1988-2017 period. As illustrated in the first section on analytical tools, the data has been log-transformed, and we are using seasonal (lag-12) differences. We estimate the model for a range of both ordinary and conventional AR and MA parameters using a rolling window of 10 years of training data, and evaluate the RMSE of the 1-step-ahead forecast.

Finding the optimal number of lags

from joblib import Parallel, delayed

from tqdm import tqdm

train_size = 120 # 10 years of training data

test_set = industrial_production_log_diff.iloc[train_size:]

def fit_and_predict(params, train_size, industrial_production_log_diff):

p1, q1, p2, q2 = params

preds = test_set.copy().to_frame('y_true').assign(y_pred=np.nan)

aic, bic = [], []

if p1 == 0 and q1 == 0:

return None

convergence_error = stationarity_error = 0

y_pred = []

for i, T in enumerate(range(train_size, len(industrial_production_log_diff))):

train_set = industrial_production_log_diff.iloc[T-train_size:T]

try:

with warnings.catch_warnings():

warnings.filterwarnings("ignore")

model = SARIMAX(endog=train_set.values,

order=(p1, 0, q1),

seasonal_order=(p2, 0, q2, 12)).fit(disp=0)

except LinAlgError:

convergence_error += 1

continue

except ValueError:

stationarity_error += 1

continue

preds.iloc[i, 1] = model.forecast(steps=1)[0]

aic.append(model.aic)

bic.append(model.bic)

preds.dropna(inplace=True)

if preds.empty:

return None

mse = mean_squared_error(preds.y_true, preds.y_pred)

return (p1, q1, p2, q2), [np.sqrt(mse),

preds.y_true.sub(preds.y_pred).pow(2).std(),

np.mean(aic),

np.std(aic),

np.mean(bic),

np.std(bic),

convergence_error,

stationarity_error]

# Parallel processing

results = Parallel(n_jobs=-1)(delayed(fit_and_predict)(params, train_size, industrial_production_log_diff) for params in tqdm(params))

# Filter out None results

results = {k: v for k, v in results if v is not None}

This version introduces parallel processing. 100% in ~14 minutes.

The following are some of the cells and their respective outputs just to show that the refactored code will not break anything that follows.

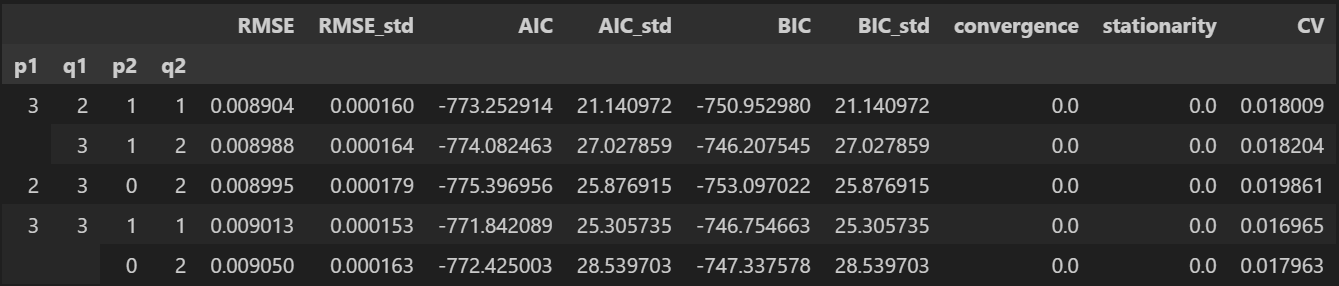

sarimax_results.nsmallest(5, columns='RMSE')

sarimax_results[['RMSE', 'AIC', 'BIC']].sort_values('RMSE').head()

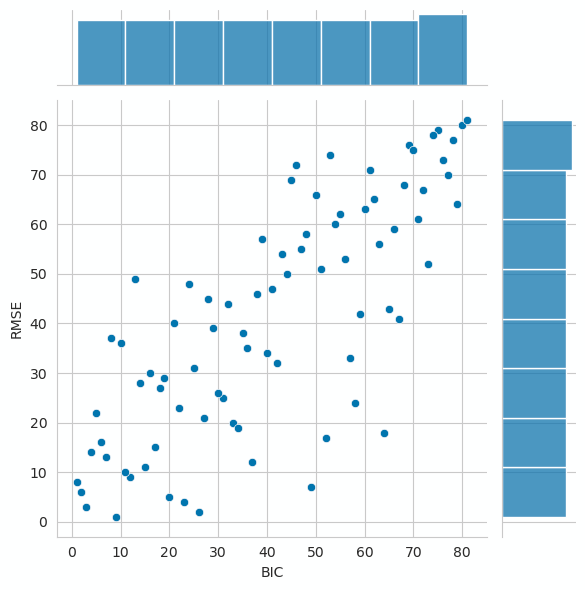

sns.jointplot(y='RMSE', x='BIC', data=sarimax_results[['RMSE', 'BIC']].rank());

.

.

.

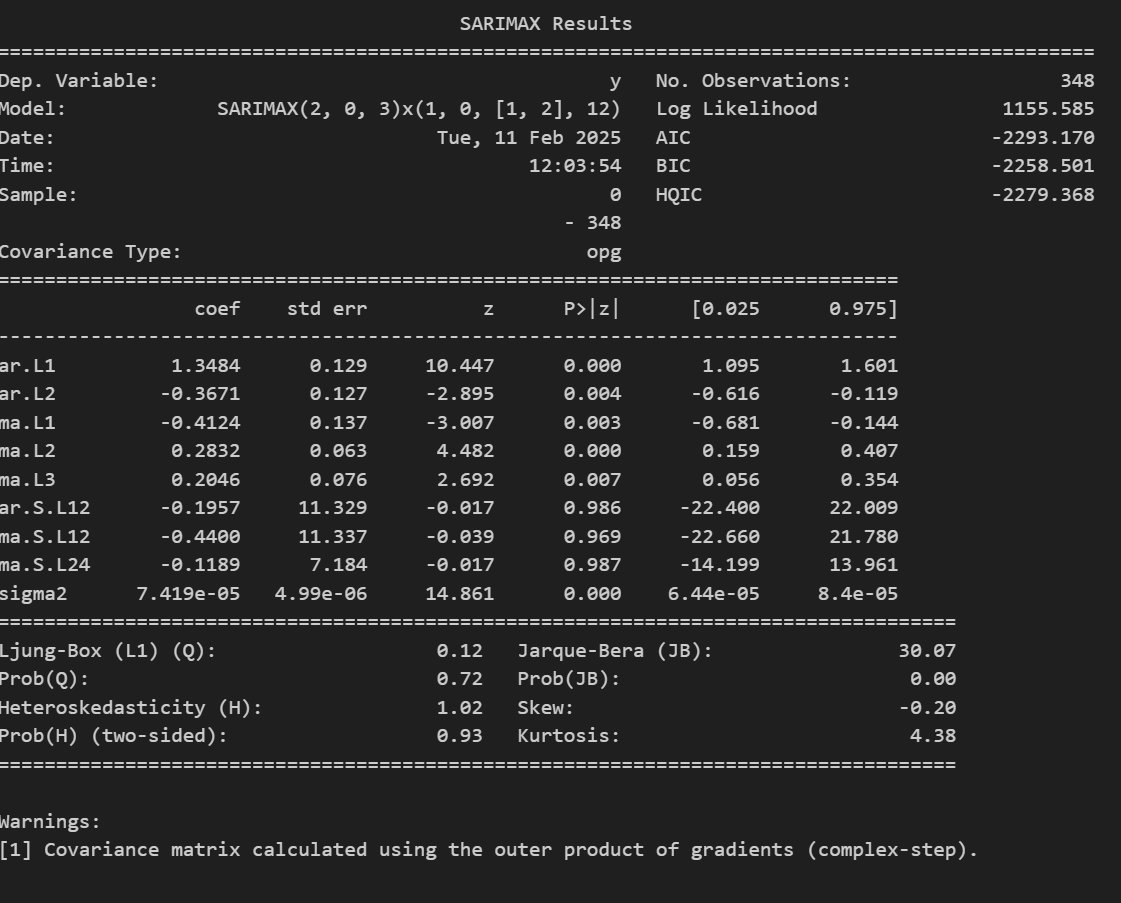

print(best_model.summary())

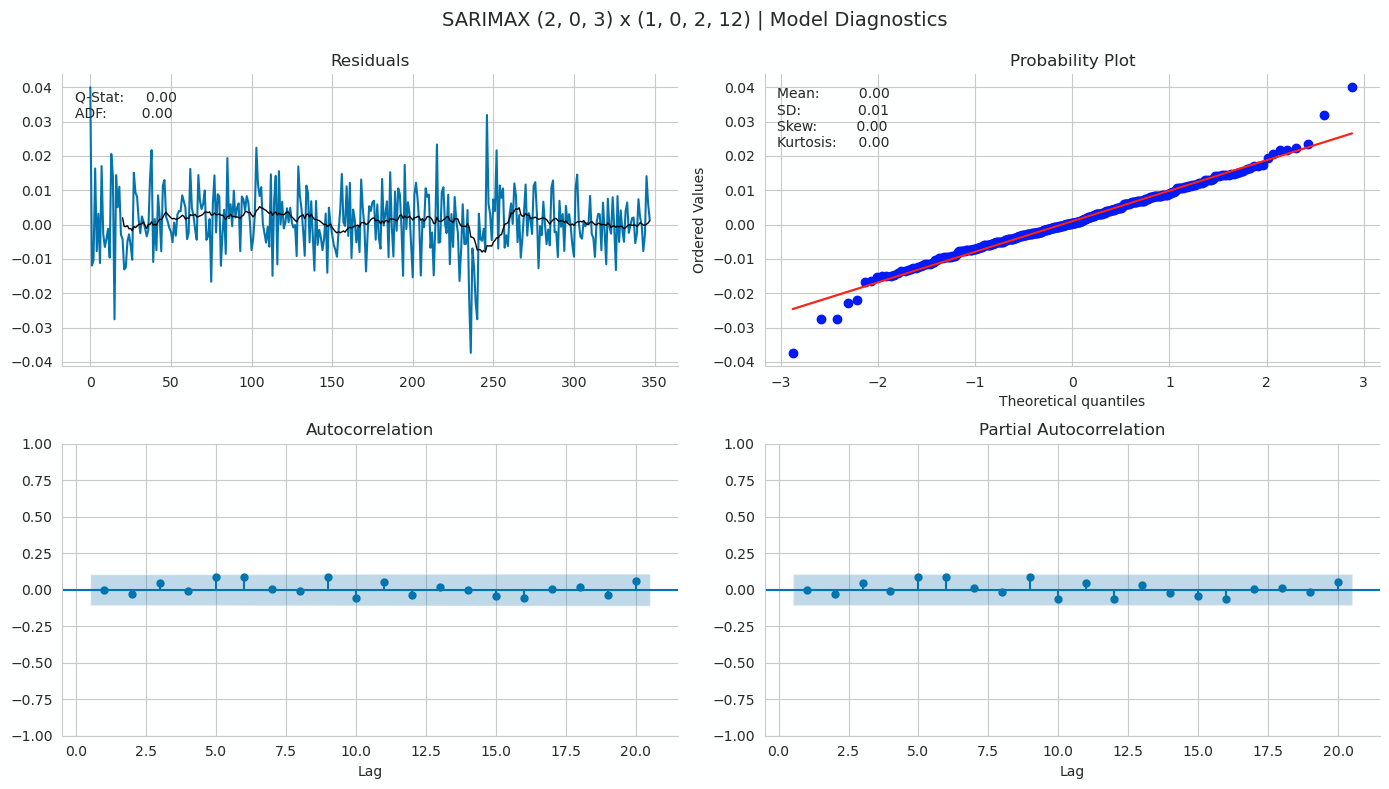

plot_correlogram(pd.Series(best_model.resid), lags=20, title=f'SARIMAX ({p1}, 0, {q1}) x ({p2}, 0, {q2}, 12) | Model Diagnostics')

Hope this helps.